3 2021 IPOs Likely To Notch Further Big Price Gains This has been a banner year for newly listed companies - and it's not over yet. So far, more than 821 companies have gone public via an initial public offering,...

By Kate Stalter

This story originally appeared on MarketBeat

This has been a banner year for newly listed companies - and it's not over yet. So far, more than 821 companies have gone public via an initial public offering, direct listing, or SPAC.

Rather than debate the pros and cons of each method of making shares available to the public, I'll stick with the tried-and-true tenet about new companies: Firms within their first few years of going public tend to be among the market's biggest price gainers.

Of course, that's not true across the board. For example, many young biotechs raise much-needed cash by going public. As they slog through clinical trials and government approvals, their stocks can languish or remain mired well below the IPO price for months or even years.

So the idea is not to blindly invest in whatever new company catches your eye; instead, it's worth tracking the fundamental and technical strength of companies new to the market.

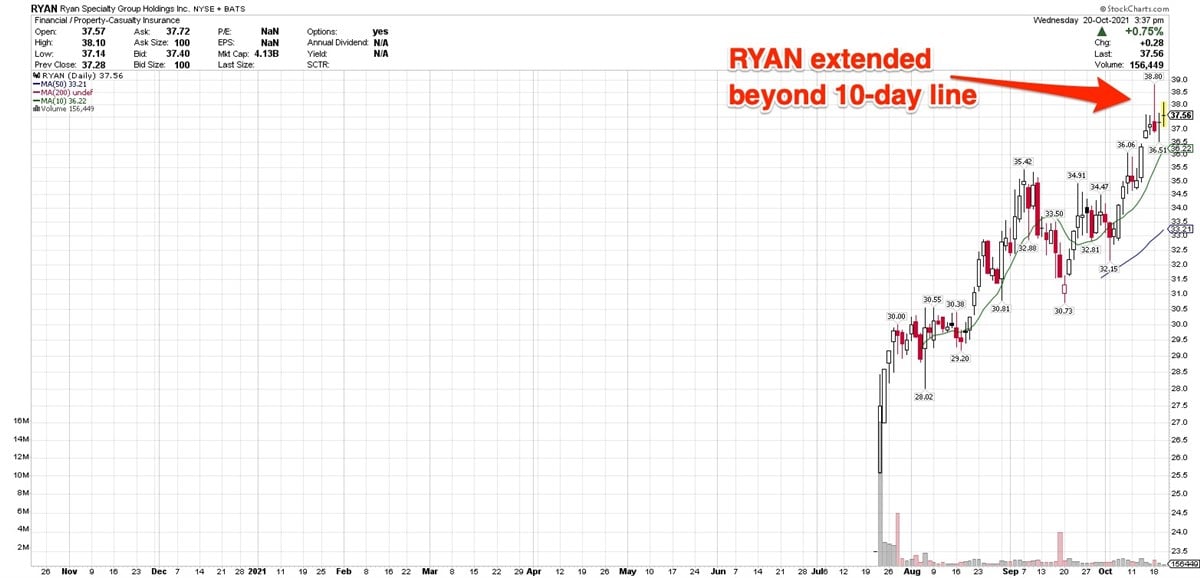

Ryan Specialty Group (NYSE: RYAN) went public on July 22 at $23.50.

Since its IPO, shares are up 61.15%, trading between $37 and $38.

Ryan is one of those companies from a decidedly non-glamorous business. The Chicago-based firm provides specialty products and solutions to the insurance industry.

Ryan Specialty Group was founded in 2010 by Patrick G. Ryan, who still serves as chairman and CEO. He has a stellar pedigree in the insurance business, having previously served as founder and CEO of AON Corporation.

Ryan Specialty Group has operations in North America, the U.K. and Europe. The company notes that its upward trajectory has been fueled through organic growth as well as acquisitions.

After its IPO, Ryan shares have been notching gains every month. It pulled into the typical post-IPO consolidation in September and early October.

The company posted double-digit revenue gains over the past five quarters. Earnings grew 100% and 71% year-over-year in the past two quarters.

For the full year, analysts expect earnings of $1.03 per share, a 203% increase.

The stock is currently extended beyond a buy point, but is one to continue watching.

Hayward Holdings (NYSE: HAYW), which went public on March 12 at $17, is up 32.18% year-to-date, despite being in a correction since early June.

Hayward manufactures swimming pool equipment, as well as cleaning and automation systems for the residential and commercial markets. The company has been around for more than 80 years.

The stock immediately went into a correction after its IPO, although it was able to notch gains in March, April, May and June.

Over the past three months, the stock declined 2.17 %, although it appears that it may be crafting the right side of its base. In the past month, shares are up 5.24%, and in the past week it's up 3.97%.

The stock is finding support along its 10-day and 21-day moving averages.

Hayward is not currently a buyable stock, as it's still working on its current consolidation. The current buy point is the prior high of $26.82, reached on May 25. The consolidation by no means is a sign that this is a stock without potential; it's just one to watch and wait for a buy point.

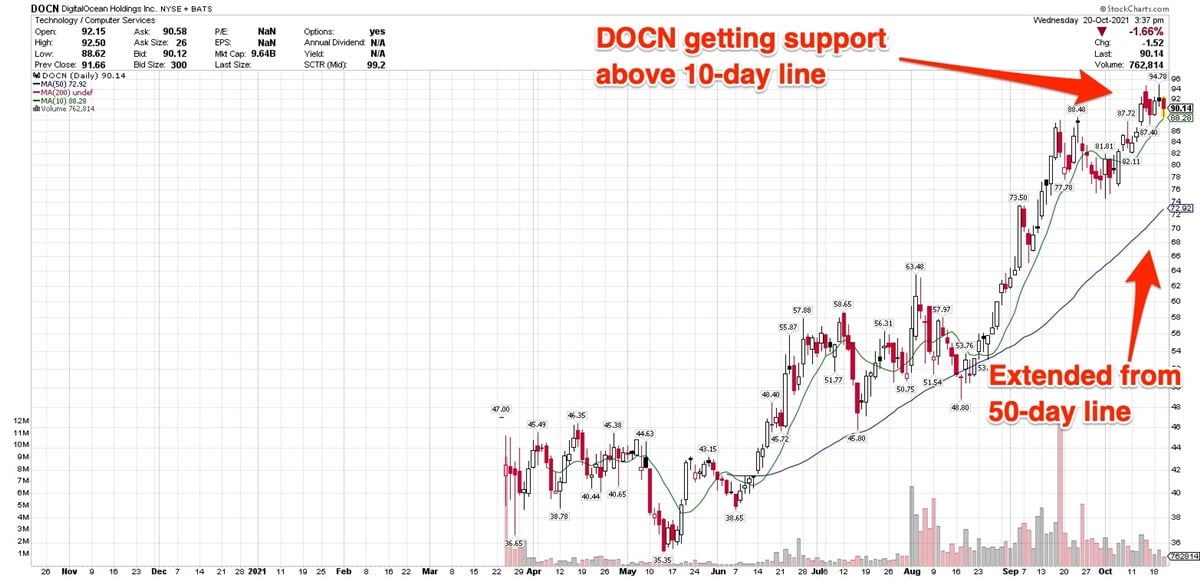

DigitalOcean (NYSE: DOCN), which went public in March at $47, is up 91.70% since its IPO. It was trading Wednesday between $90 and $91.

The New York-based company offers a range of cloud computing services to business customers. It focuses on developers, start-ups, and small- and medium-sized businesses in North America and internationally.

It's very typical for a stock to pull into a correction soon after its IPO, and that's exactly what DigitalOcean did. It went on to form another choppy consolidation starting in July, but it's been remarkably consistent finding support above its 50-day moving average.

That's a good sign that institutional investors are maintaining support for the stock even during pullbacks, even adding some shares at a lower price, rather than selling out en masse.

Analysts expect the company to turn profitable this year, earning $0.28 per share. That's seen rising to $0.57 per share in 2022, a gain of 104%.

This stock is potentially buyable at this juncture, as it's pulled back from Tuesday's all-time high of $94.78. However, it's currently 24.1% above its 50-day moving average. A pullback with support at that line would likely offer a better chance to get in at a lower price, without sitting through a correction soon after a purchase.