3 Stocks Getting Upgrades With the S&P 500 index currently down 10% from its all time high and struggling to get its mojo back, it can be a scary time for investors trying to...

By Sam Quirke

This story originally appeared on MarketBeat

With the S&P 500 index currently down 10% from its all time high and struggling to get its mojo back, it can be a scary time for investors trying to pick new stocks. Aside from sitting on your hands and waiting for the volatility to subside, one of the better and more reliable ways to filter out the junk from the quality is by looking at recently upgraded stocks. These are companies that the major sell-side firms think are currently under-valued and that offer some tempting upside.

Let's take a look at three such stocks that have recently been upgraded.

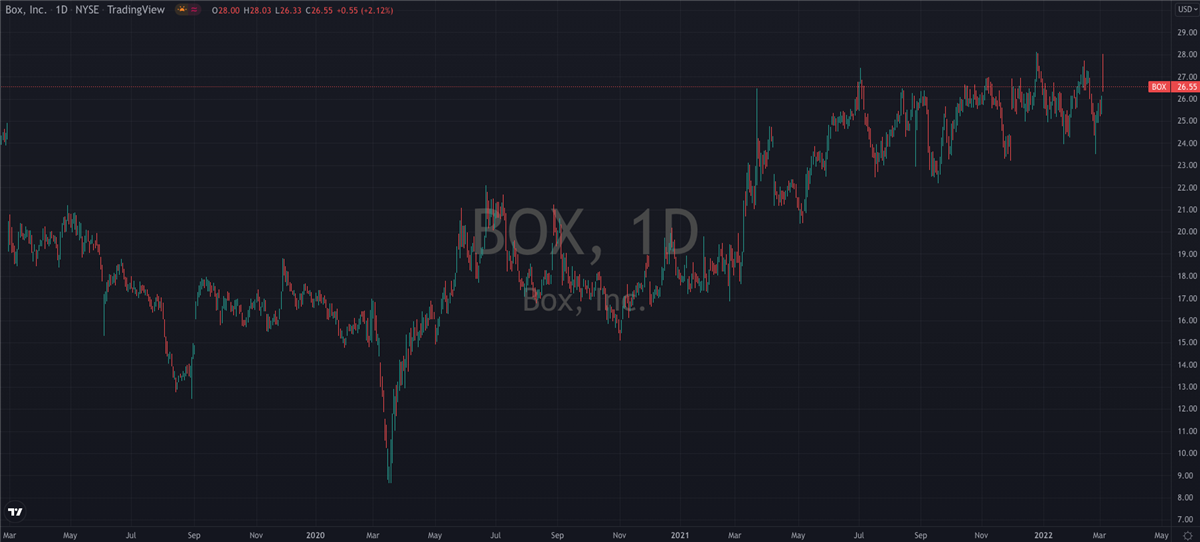

Box (NYSE: BOX)

The fact that Box shares are currently at multi-year highs tells you a lot about their potential to keep rallying in the face of a recent upgrade. The team over at J.P. Morgan upped their rating on the cloud content company yesterday after the Redwood City headquartered Box delivered a solid beat on their Q4 earnings. Both EPS and revenue came in ahead of analyst expectations, the latter showing year on year growth of 17% while it did so.

Analyst Mark Murphy upped his rating from Underweight in light of the results, noting that the business is accelerating, as evidenced by the most recently reported results. While stiff competition from the likes of Microsoft (NASDAQ: MSFT) and others still exists, Box has improved its profitability "markedly" since their shares were downgraded to Underweight more than two years ago.

Box shares are right at the top of their recent range and within touching distance of kicking on to their highest levels since 2018. In a note to clients, Murphy wrote "as Box embarks on revenue acceleration into the low-to-mid teens with expanding margins and improving churn, we see the risk reward as much more balanced at current price levels, informing our rating change".

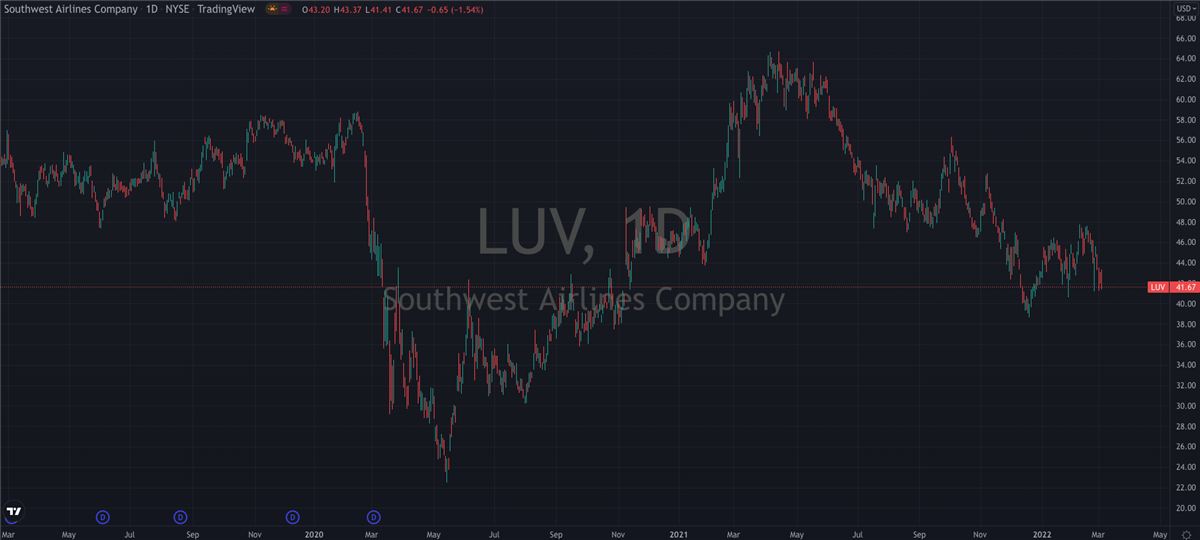

Southwest Airlines (NYSE: LUV)

Despite the airline and travel industry still looking bedraggled from the COVID pandemic, Southwest Airlines have been named again and again in recent months as one of the best-looking majors still flying. That being said, their shares are currently trading 35% lower than where they were a year ago, but there's a new bull voice saying that now might be the right time to buy.

Evercore ISI were out with a surprise upgrade yesterday as they upped their rating on Southwest to Outperform. In a note to clients, they said "while reliability remains a priority, Southwest appears margin recovery-focused and must be considering the volatile inputs that the rest of the world can see too. Greater relative financial strength and margin-focused planning lead us to raise our rating."

This is just what investors in Southwest needed to hear, and you can be sure the comments will have attracted the attention of more than a few who are on the sidelines. Having survived the worst of the pandemic, airlines stocks lost whatever strength they had in their bid last week after Russia invaded Ukraine. But for investors with a long enough time horizon, the combination of this recent upgrade and the company's Q4 results from late January, which had revenue up 150% on the year, should be enough to justify an entry.

Take-Two (NASDAQ: TTWO)

Take-Two is another of the pandemic darlings that's suffering from a post-pandemic hangover. After peaking just over a year ago, their shares find themselves down 25%. Video game sales have fallen for three months in a row and the multi-month run of rising sales has been firmly broken. But investment firm MKM Partners upgraded the stock yesterday, citing what they called a "very compelling growth story."

Analyst Eric Handler upped his rating from Neutral to Buy, and slapped a fresh price target of $200 on the shares. Were they to hit this, they'd be within a few dollars of last year's all-time high and would have rallied more than 25% to get there in the meantime. This is the kind of upside that investors find hard to ignore, and it's reasonable to expect a bid to appear in Take-Two shares next week on the back of it.

Referring to the company's recent acquisition of Zynga, Handler also noted that "if Take-Two can effectively execute, the $200 price target could be conservative, as earnings per share could be aided between 17% and 30% from Zynga in 2024. There could also be about $100 million of cost synergies and roughly $500 million of top line synergies over time, which are likely to be evident in 2025."