Banks Aren’t Your Friends

There is that person in everyone’s life. No matter who it is, like a relative or friend, we do not want to lend money to them. Why? Because we know…

Due - Due

This story originally appeared on Due

There is that person in everyone’s life. No matter who it is, like a relative or friend, we do not want to lend money to them. Why? Because we know we won’t be repaid if we lend them money.

After all, who in their right mind would loan someone money if they didn’t have any cash on hand? They don’t have a rainy day fund. Their emergency fund is non-existent. And, they have zero reserves.

So why would you put yourself through this?

Well, the same idea applies to keeping all of your money in the bank.

Bank’s Primary Purpose

This is a simple question. What are banks for? Answers you might get include paying bills, saving money, funding businesses, funding government, managing risk, building communities, ensuring people’s safety, and enabling trade. These answers are all true — to an extent. But, banks aren’t your friend. Banks are a business.

Their goal, whether it’s a credit union, big bank, or small bank is to get you to become a customer. Once you have a free checking or savings account, they can market other products to you. It’s the same thing as all the investment companies out there. As their customer, they want you to open up a Roth IRA and begin investing. And, they’ll start marketing other stuff to you once they get to know you.

In other words, like any other business, once your walk through the door, they begin to look for ways to make money off you. This is what’s called monetizing every single relationship.

And, look. There’s nothing wrong with that. A banking account is a necessity. But, where people miss the mark is that they keep all of their money in the bank.

Like you, this was the trap that my parents fell in. Growing up, they told me time and time again to save money. All you have to do is open your free account. And, they pay you a certain interest rate. And, they were fine with that instead of building a diversified portfolio or working with an investment firm.

If you have a lot of cash in your bank account, you will feel more secure. On the other hand, it can be harmful if you’re not careful. Specifically, if you’re treating a checking account as a savings account or solely for investing.

How Banks Make Money

So, if a bank is a business, then how do they turn a profit?

The biggest source of money for banks is deposited money. This money that account holders transfer to the bank for safekeeping and future use — plus a little interest on top.

A lot of people still have checking and savings accounts today, which are commonly referred to as ‘core deposits. Deposits into CDs and money market accounts are also common.

Deposited funds are then used by banks to lend money to other customers. The customer, however, reserves the right to withdraw the full amount at any time. If you withdraw your money from a CD before it matures, you might be hit with a penalty.

Additionally, banks make money from interest — whether it’s a small business loan, a mortgage, or a line of credit. Your interest rate will be higher if your credit score isn’t the best. As an example, the average interest rate for unsecured loans is around 10 percent for those with great credit, whereas the rate for those with poor credit can range between 18 percent and 36 percent.

Infuriatingly, banks make money through fees, mainly by charging ATM and overdraft fees. According to the Consumer Financial Protection Bureau, U.S. banks collectively generate about $15 billion in overdraft and NSF fees a year!

Let’s talk about fractional reserve banking.

Remember your broke friend or relative that you just wouldn’t feel right lending money to? Well, if you do loan them, knowing that that won’t pay you back? Well, then this isn’t a loan. It’s a gift.

Most people are familiar with FDIC insurance. This is the insurance that protects you in the event that, if the bank were to go bankrupt, you wouldn’t lose everything. Or, if something catastrophic happens, you have some kind of insurance protecting your deposit.

However, many people are unaware that banks must typically keep a certain percentage of their deposits in reserve. This is known as fractional reserve banking. Basically, this means that banks are supposed to keep a certain percentage of the deposits they have on hand as reserves.

For example, let’s assume the bank has a hundred million dollars in deposits. They need to have that amount of cash on hand. And, in a way, this is no different than having an emergency fund. Financial experts typically recommend having 3 to 6 months’ cash on hand in case of an emergency. That is your cash reserve that is there in case you need it.

Also, based on the size of the bank, a cash reserve is required. The FED required banks with assets between $16 and 124 billion to hold 3% in reserves. Anything bigger than $124 million was 10%.

In any case, you should remember that banks invest your money. And you have no clue where that money goes. And, unfortunately, you don’t get all this information whenever you open up your free checking account or CD. The bank is not going to offer any of this information. But this is information that you need to know if you have money in the bank.

Federal reserve requirements = ZERO.

When depositors made many withdrawals during the Great Depression, it led to bank runs. Therefore, the fractional banking system was established. Depositors’ funds are protected against risky investments by the reserve requirement developed by the government.

Reserves are kept in banks’ vaults or at Federal Reserve Banks near them. Reserve requirements are established by the Board of Governors of the Fed and are one tool used to guide monetary policy. Commercial banks with deposits under $15.2 million are exempt from maintaining reserves as of January 2016.

Again, banks with deposits from $15.2 to $110.2 million were required to keep their reserve requirements at 3%, while banks with deposits over $100.2 million were required to keep their reserve requirements at 10%.

However, the FED pretty much took away this title during the pandemic.

What does that money do? Well, let’s say everyone tried to withdraw funds from their bank accounts. Well, the banks don’t have that cash on hand. In short, you can’t get your money.

I know that sounds wild. But, remember. Banks don’t want everyone to make withdrawals. They want you to keep your money in the account to make money off you.

Banks Aren’t Designed to Build Wealth

Okay. Enough with that fearmongering. It’s unlikely that everyone with a bank account would make a run like the one that set off the Great Depression. However, if you have all of your money in a single bank account, that particular bank might have the cash on hand to accommodate your request.

So, like lending money to your broke friend or family member, without that security, you aren’t getting that money back.

But, there’s another problem. You aren’t making money by parking all of your cash in a bank account.

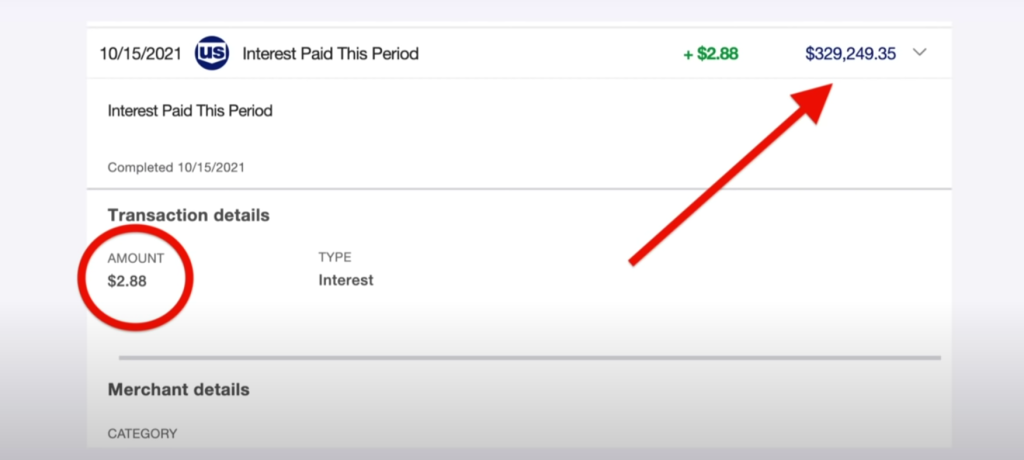

I’ll give you an example. I’ve got almost $330,000 in a savings account. Guess how much interest I made in a month? $2.88. Let me repeat. Two dollars and eighty-eight cents.

As I’ve written before, you’re losing money at your bank. Why? Because banks often pay low-interest rates on savings accounts. Currently, interest rates are at 0.06% and inflation is at 5%.

I can’t stress this enough. It’s better for financial institutions to have a higher borrowing rate than to pay savings account holders. It’s for this reason that savings account rates are so low. In order to make money on loans, banks keep their interest rates low so they can keep making free money on savings accounts.

Yeah. Banks be playing you.

Instead of getting played though, consider other options, such as;

- Neobanks.

- Treasury Inflated Protected Securities.

- Online investment apps.

- High yield bonds.

- High yield stocks.

- Real estate investment trusts.

- Short-term notes.

I’d also recommend low-risk investments with high returns. I’m talking about high-yield savings accounts, dividend-paying stocks, and annuities.

Banks Do Have a Purpose

I have trashed banks up to this point. To be fair though, their behavior when it comes to investing is certainly deserved. When they do, they usually give bad advice since most aren’t qualified to give it.

Banks do, however, serve an important purpose in your financial plan. In general, banks are a good place to store money for an immediate financial need — such as saving for a house or a car. Also, they’re a good choice for emergency funds, since those have to be safe and liquid.

Banks are excellent at this, and they need to stay focused on it. However, local banks aren’t always the best option. They pay too low-interest rates.

In general, you are better off saving for any of these purposes with an online bank. BBVA Compass, CIT Bank, and Ally Bank are examples. Often, they have a higher interest rate.

Definitely use banks for those purposes. Investing, however, requires thinking beyond banks. Most are not suited to handling investments, and those that usually charge excessive fees.

If you are considering investing your money, rethink your bank plan. After all, banks are terrible for investing.

Frequently Asked Questions

1. How much money should you keep in the bank?

There’s no right or wrong amount for you to keep in your bank account. It varies depending on several factors like your monthly expenses and cash flow.

To account for your money’s ebbs and flows, Stash Wealth recommends a $2,000 to $3,000 cushion at most in your checking account. However, if you don’t have a lot of expenses, that number might seem high. For a more accurate amount, add your monthly expenses. After that, set a cushion that doesn’t make you feel jittery until payday.

A good rule of thumb for savings accounts is three to six months of expenses. What if you work in a stable industry, are healthy, and live in a low-cost area? Depending on your situation, you may only need a small emergency fund.

2. Why do people invest with banks?

Many people like to keep their money safe, no doubt. And, banks seem to be the safest bet. After all, your deposits are insured by the FDIC.

However, even FDIC insurance has limitations from an investment standpoint. Your money is only insured for up to $250,000 per depositor. Although that might seem like a lot of money, if you’re going to invest for the long term — and especially when it comes to retirement accounts — you need to set your sights on much higher balances, at least eventually.

Another limitation of FDIC insurance is that it only covers bank deposits. Such accounts include checking, savings, and money market accounts, as well as certificates of deposit.

The FDIC does not cover funds in investment accounts held by banks. This fact is clearly conveyed in the fine print on bank investment accounts. Stocks, bonds, mutual funds, and other true investment assets are not covered by the FDIC as well.

However, the problem lies in public perception. An investor may be reassured of the safety of their investments because of FDIC insurance. Your money is not safe if it is invested in anything other than bank deposits.

Banks are also likely to be attractive to some investors for their brick-and-mortar locations. Although most investing has moved online, there is still a sense that having physical branches is somehow safer than having few or no locations. However, perceptions are not reality. For this reason, you won’t find value in investing through your bank.

3. Do I need to keep a certain amount of money in my account?

Opening an account at a bank typically requires a deposit. Some banks charge fees if an account does not maintain a minimum or average balance. However, certain conditions may waive the fee.

4. Does the bank account pay me interest?

Checking accounts usually offer low-interest rates if they pay interest. In exchange for the higher interest, high-yield checking accounts typically require larger balances.

A savings account offers a higher interest rate, but because the account is designed to be saved, it has different rules. Several banks may charge customers for frequent savings withdrawals as a result of federal regulations, which apply to all banks.

When you’re determining what type of account you’ll use, it’s always a good idea to check the deposit agreement and any disclosures. This way you can see what applies. Generally, this can be done while you’re looking at interest rates.

5. Can I withdraw all of my money from a bank account?

According to federal law, you are permitted to withdraw as much cash as you want from your bank account. After all, it’s your money. You might be asked why you need so much cash if you withdraw more than a certain amount, however. Also, the withdrawal will probably be reported to Uncle Sam.

There are some other considerations as well. For example, if you withdraw a million bucks, your local branch might not have that on hand. So, you should give them a head’s up. Also, if you empty your account, the bank may also close it.

The post Banks Aren’t Your Friends appeared first on Due.

There is that person in everyone’s life. No matter who it is, like a relative or friend, we do not want to lend money to them. Why? Because we know we won’t be repaid if we lend them money.

After all, who in their right mind would loan someone money if they didn’t have any cash on hand? They don’t have a rainy day fund. Their emergency fund is non-existent. And, they have zero reserves.

So why would you put yourself through this?