Verint Systems Stock is a Customer Engagement Play

Customer engagement software provider Verint Systems (NASDAQ: VRNT) stock has been resilient trading down (-17%) on the year compared to (-26%) for the Nasdaq 100 index.

MarketBeat.com - MarketBeat

This story originally appeared on MarketBeat

Customer engagement software provider Verint Systems (NASDAQ: VRNT) stock has been resilient trading down (-17%) on the year compared to (-26%) for the Nasdaq 100 index. The Company is a benefactor of the cloud migration and digital transformation trend that continues to accelerate. The workforce engagement management is a growing field that plays right into Verint’s wheel house as enterprises seek to optimize workflows and talent performance. Cloud revenues grew at over 30% and the Company signed over net 100 new logos in fiscal Q1 2023 as it transitions to the cloud SaaS model. Verint seeks to close the capacity gap for brands as macroeconomic headwinds become more challenging including wage inflation, talent recruitment, and optimizing workflow management in the post-pandemic hybrid workforce. Utilizing AI capabilities and automation to help improve the customer experience and optimize workflows is driving strength across all key cloud metrics. Prudent investors looking for exposure a company that benefits from cloud, customer engagement and workflow optimization tailwinds can look for opportunistic pullbacks in shares of Verint Systems.

Fiscal Q1 2023 Earnings Release

On June 7, 2022, Verint released its fiscal first-quarter 2023 results for the quarter ended April 2022. The Company reported earnings-per-share (EPS) profits of $0.52 versus a profit of $0.47 consensus analyst estimates, an $0.05 beat. Revenues grew 8.6% year-over-year (YoY) to $219.25 million, beating analyst estimates for $215.52 million. Verint Systems CEO Dan Bodner commented, “I am pleased to report strong cloud momentum in the first quarter with revenue and diluted EPS coming in ahead of expectations. Our first quarter showed strength across all key metrics including New Perpetual License Equivalent (PLE) Bookings growth and mix, with our bookings continuing to shift to SaaS. Looking ahead, we expect our cloud momentum to continue and are raising our annual guidance for cloud revenue growth to a range of 32% to 34%. Behind our strong momentum is our focus on helping brands close the engagement capacity gap with our highly differentiated customer engagement cloud platform.”

Reaffirms Guidance

The Company reaffirmed guidance for fiscal full-year 2023 for EPS of $2.50 versus $2.51 consensus analyst estimates. The Company sees fiscal full-year 2023 revenue between $921.2 million to $958.8 million versus $944.11 million consensus analyst estimates. Cloud revenue growth is expected between 32% and 34% YoY.

Conference Call Takeaways

CEO Bodner believes cloud momentum will remain strong as they raise annual guidance by 200 basis points to a range of 32% to 34%. It’s differentiated customers engagement cloud platform has become more urgent for companies especially in light of recent macroeconomic conditions. The Company helps brands reduce costs and elevate customer experiences. Cloud revenues continue to accelerate growing 38% YoY as the mix continues to shift to the cloud. New PLR bookings rose 27% YoY. The Company also received 26 cloud orders that exceed $1 million total contract values including notable brands like Comcast, Marriott, Zillow, and Wells Fargo. The Company added over 100 new logos including NVIDA, Eastman Chemical, St. John’s University and KinderCare. He highlighted some notable wins in the quarter including a $15 million contract from a leading insurance company and a $3 million order from a healthcare company.

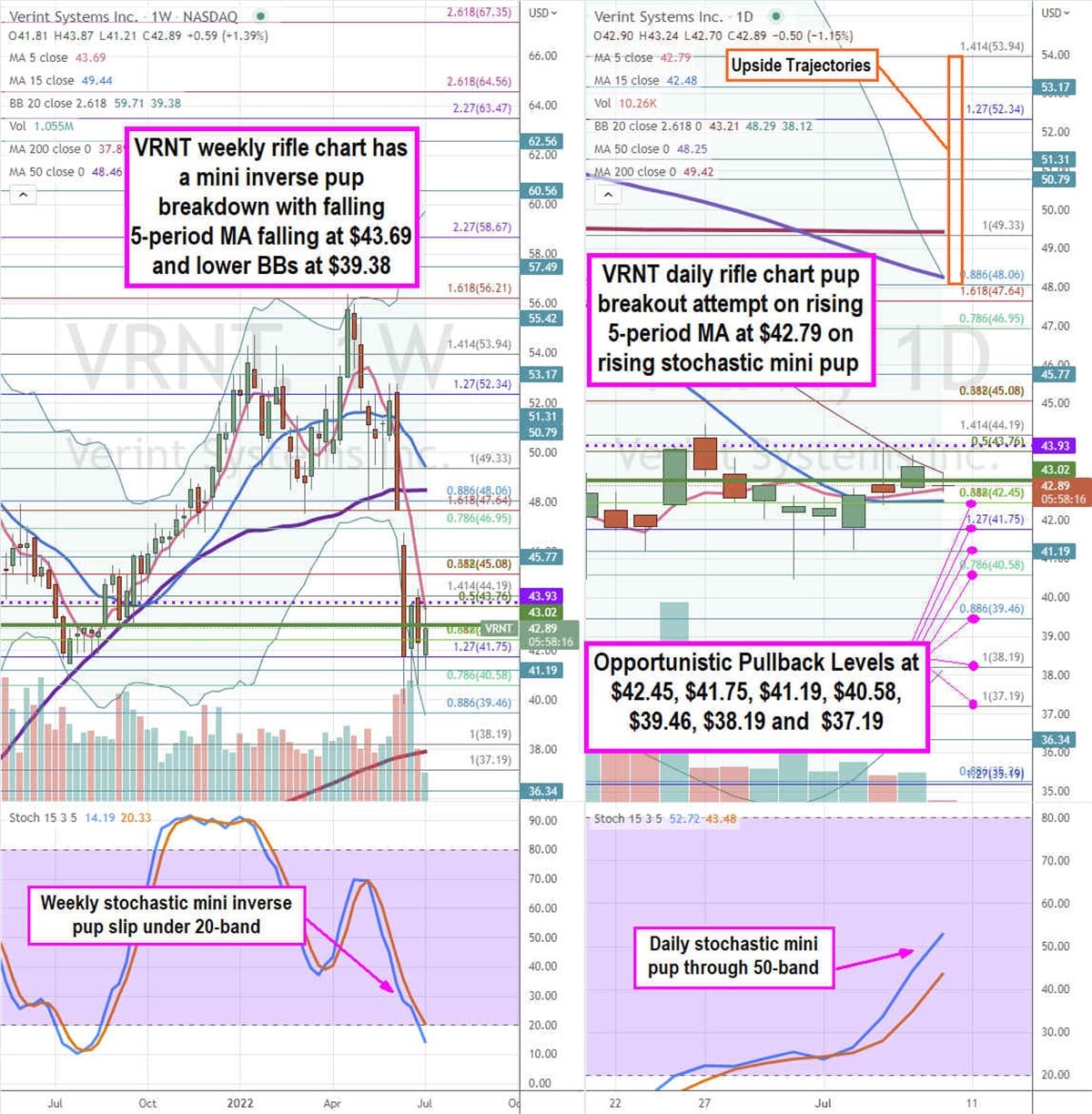

VRNT Opportunistic Pullback Levels

Using the rifle charts on the weekly and daily time frames provides a precision view of the landscape for VRNT stock. The weekly rifle chart triggered a mini inverse pup breakdown on the rejection off the $44.19Fibonacci (fib) level as it leaned near the $39.46 fib level before staging a bounce. The weekly 5-period moving average (MA) is falling at $43.69 followed by the 15-period MA at $49.44 with weekly lower Bollinger bands (BBs) at the $39.46 fib. The weekly stochastic formed a mini inverse pup falling through the 20-band. The weekly market structure low (MSL) buy triggers on the breakout above $42.89. The daily rifle chart is attempting a breakout with a tight channel as the 5-period MA rises at $42.79 followed by the 15-period MA at $42.48. The daily upper BBs overlap with the daily 50-period MA at $48.29. The daily stochastic formed a mini pup rising through the 50-band. Prudent investors can look for opportunistic pullbacks at the $42.45 fib, $41.75 fib, $41.19, $40.58 fib, $39.46 fib, $38.19 fib, and the $37.19 fib level. Investors can also watch a lead cloud SaaS peer Salesforce (NASDAQ: CRM) to gauge sentiment.

Customer engagement software provider Verint Systems (NASDAQ: VRNT) stock has been resilient trading down (-17%) on the year compared to (-26%) for the Nasdaq 100 index. The Company is a benefactor of the cloud migration and digital transformation trend that continues to accelerate. The workforce engagement management is a growing field that plays right into Verint’s wheel house as enterprises seek to optimize workflows and talent performance. Cloud revenues grew at over 30% and the Company signed over net 100 new logos in fiscal Q1 2023 as it transitions to the cloud SaaS model. Verint seeks to close the capacity gap for brands as macroeconomic headwinds become more challenging including wage inflation, talent recruitment, and optimizing workflow management in the post-pandemic hybrid workforce. Utilizing AI capabilities and automation to help improve the customer experience and optimize workflows is driving strength across all key cloud metrics. Prudent investors looking for exposure a company that benefits from cloud, customer engagement and workflow optimization tailwinds can look for opportunistic pullbacks in shares of Verint Systems.

Fiscal Q1 2023 Earnings Release

On June 7, 2022, Verint released its fiscal first-quarter 2023 results for the quarter ended April 2022. The Company reported earnings-per-share (EPS) profits of $0.52 versus a profit of $0.47 consensus analyst estimates, an $0.05 beat. Revenues grew 8.6% year-over-year (YoY) to $219.25 million, beating analyst estimates for $215.52 million. Verint Systems CEO Dan Bodner commented, “I am pleased to report strong cloud momentum in the first quarter with revenue and diluted EPS coming in ahead of expectations. Our first quarter showed strength across all key metrics including New Perpetual License Equivalent (PLE) Bookings growth and mix, with our bookings continuing to shift to SaaS. Looking ahead, we expect our cloud momentum to continue and are raising our annual guidance for cloud revenue growth to a range of 32% to 34%. Behind our strong momentum is our focus on helping brands close the engagement capacity gap with our highly differentiated customer engagement cloud platform.”

Reaffirms Guidance