2 Tech Stocks to Buy During the Market Correction It's been a volatile start to the year for the major market averages, and the Nasdaq 100 Index (QQQ) has been the weaker index, sliding more than 18% from its...

By Taylor Dart

This story originally appeared on StockNews

It's been a volatile start to the year for the major market averages, and the Nasdaq 100 Index (QQQ) has been the weaker index, sliding more than 18% from its highs. Since its January low, the ETF has recovered nearly half of its gains, rallying 10% following an extremely oversold reading on January 24th. Paypal (PYPL) and AMD (AMD) are two top tech stocks that investors should look to buy on the pullback.

It's been a volatile start to the year for the major market averages, and the Nasdaq 100 Index (QQQ) has been the weaker index, sliding more than 18% from its highs. Since its January low, the ETF has recovered nearly half of its gains, rallying 10% following an extremely oversold reading on January 24th. This has led to a spike in bullish sentiment, with the fear and brief panic from two weeks ago now replaced with some greed and belief that the market is headed back to new highs in short order.

Given this shift in sentiment and the strong oversold bounce we've seen, I believe it's more likely that the Nasdaq-100 could re-test its lows and even undercut its January 24th low before the correction is finally over. However, this is a great time to prepare a buy-list in case the market does undercut its low, given that this allows one to act if the time comes vs. scrambling to find ideas amid the volatility when it can be challenging to pull the trigger. In this update, we'll look at two names that look very reasonably valued if we see further weakness over the coming weeks.

(Source: TC2000.com)

The Q4 Earnings Season has certainly been eventful in the tech space, with very bifurcated results among different names. Advanced Micro Devices (AMD) is one name that posted another strong quarter of exceptional performance and has rallied sharply from its lows since the announcement. Meanwhile, PayPal (PYPL) reported mediocre results but ghastly guidance, reeling in its previous growth estimates.

In PYPL's case, the decline below $150.00 was justified. However, the stock is down another 18% since its violation of the $150.00 level. In AMD's case, the stock looks too cheap if it can continue to post blowout results and is one of the few examples of growth at a reasonable price. This is evidenced by its impressive 59% compound annual EPS growth rate if it can meet FY2023 annual EPS estimates. Let's take a closer look at both companies below and their respectively low-risk buy points:

Beginning with PayPal, its most recent quarter was one of the worst we've seen since the Tech Earnings Season began, with revenue coming in at ~$6.92BB, translating to just 13% growth year-over-year. This translates to a 2-year average sales growth rate of 18%, which certainly made it difficult to justify the stock's premium multiple. However, it was the company's guidance that was unpalatable. This is based on an FY2022 guide with total payment volume expected to grow just 19%, revenue expected to grow only 16%, and annual EPS projected to grow just 2% year-over-year.

As PYPL's historical earnings trend shows below, the company has historically grown annual EPS at a compound annual growth rate of ~23.4%, which is exceptional and has made it one of the market leaders in the FinTech space. However, after plugging in FY2022 estimates of $4.69, this compound annual EPS growth rate is expected to decelerate by nearly 350 basis points year-over-year. This is the last thing that the market wants to see, especially for a company that's commanded a premium multiple. Hence, the sharp sell-off in the stock should not be overly surprising.

(Source: FactSet.com, Author's Chart)

The good news is that while FY2022 is expected to be a softer year, annual EPS is projected to bounce back in FY2023, with analysts comfy with estimates between $5.65 and $5.95, or an average estimate of $5.79. Even in the middle of this range, this would translate to a slight improvement in PYPL's future compound annual EPS growth rate (20.5%) and a minor sequential uptick. Obviously, the key will be meeting these estimates, but if the company can meet or beat these estimates, much of the negativity looks to be priced into PYPL.

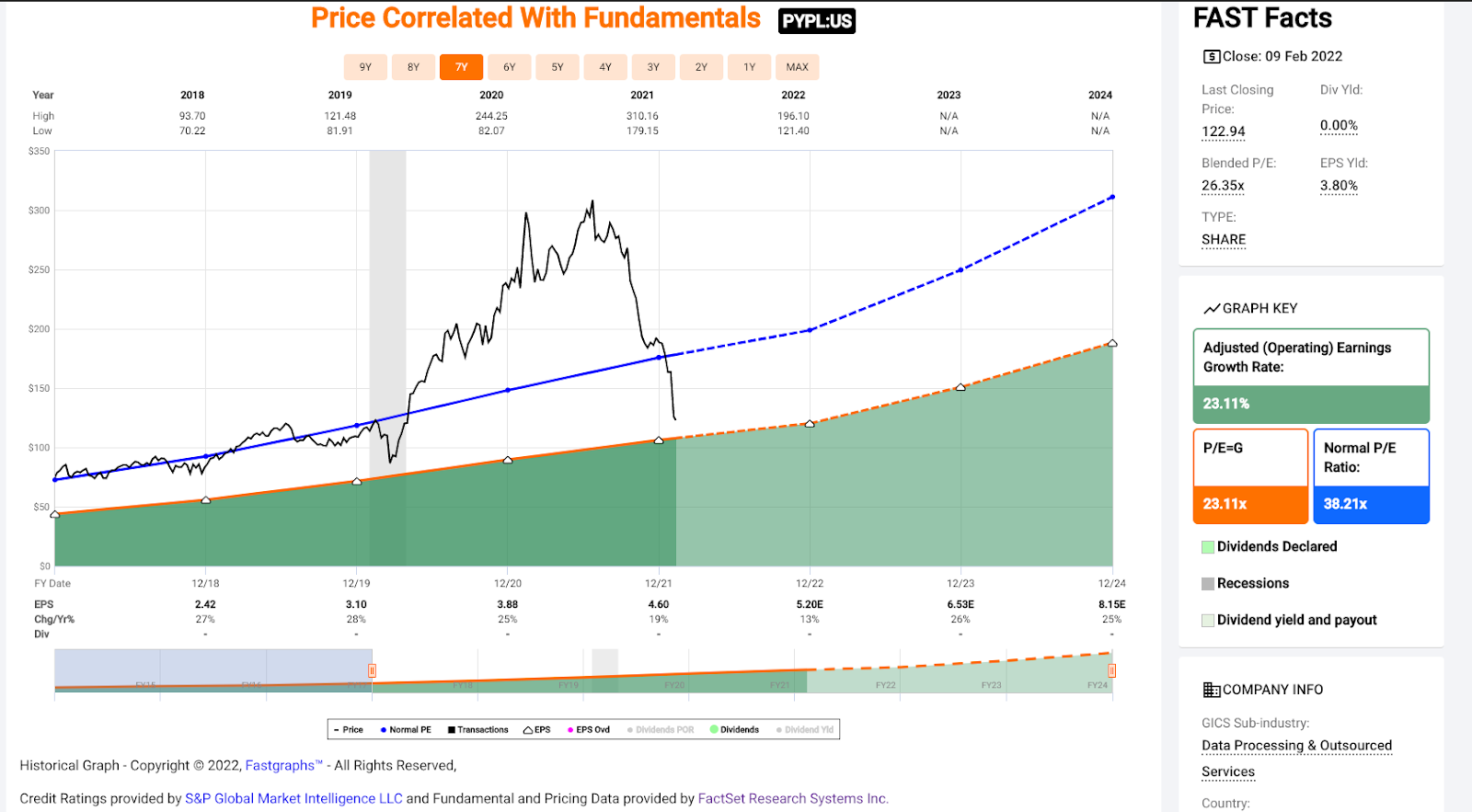

(Source: FASTGraphs.com)

Looking at PayPal's valuation above, we can see that it has historically traded at between 38-40x earnings and currently trades at just ~21.4x FY2023 earnings estimates at a share price of $124.00. Given the deceleration in the growth rate we've seen, I do not believe it makes sense to assume that PYPL would continue to command a multiple similar to its higher growth years. Therefore, I believe a more conservative multiple is 27.

However, even under conservative assumptions (27 multiple and $5.70 in FY2023 annual EPS), PayPal's fair value comes in at $153.90. This points to a 24% upside from current levels and bakes in a meaningful margin of safety. It's also worth noting that after this waterfall decline, the stock has found itself backtesting a major breakout level at $121.00, with no meaningful resistance until $179.00. With the stock having less than $3.00 in downside to support and more than $50.00 in upside to resistance, any pullbacks below $120.00 should offer an attractive entry point for long-term investors.

(Source: TC2000.com)

Moving over to Advanced Micro Devices, we saw the near opposite, with AMD reporting blowout results. The company's Q4 sales came in at $4.83BB, up 49% year-over-year, which crushed estimates by more than $300MM or nearly 7%. Meanwhile, quarterly EPS soared to $0.92, up 77% year-over-year and 20% above estimates of $0.76. This was helped by a phenomenal quarter with higher average selling prices due to a favorable product mix with Ryzen processor sales and strong demand for premium desktop and notebook PCs built with Ryzen 5000 processors.

Meanwhile, in its Enterprise, Embedded, and Semi-Custom segment, revenue soared 75% year-over-year and 17% sequentially due to higher EPYC and semi-custom processor sales, while operating income improved due to sales leverage and a favorable product mix. This combination of margin expansion (50% vs. 45%) and strong revenue growth helped AMD grow quarterly earnings per share nearly in line with last quarter's growth (78%) and more than 110% year-over-year ($2.79 vs. $1.29). So, while AMD may have looked pricey at 100x FY2020 earnings, it now trades at just 47x trailing earnings.

(Source: YCharts.com, Author's Chart)

If we look at AMD's earnings trend above, we can see that while FY2021 was an incredible year, this growth is set to continue. This is based on FY2022 and FY2023 estimates sitting at $3.96 and $4.68, respectively, forecasting 67% growth in annual EPS over the next two years. If these estimates are met, this will give AMD an industry-leading compound annual EPS growth rate of 59%, which is well above its historical average. Based on what I believe to be a conservative earnings multiple of 40, and FY2023 annual EPS estimates of $4.68, this points to further upside, with a fair value closer to $187.00.

(Source: TC2000.com)

However, while AMD remains reasonably valued at $132.00, the stock has just rallied more than 20% off its recent lows, and often sharp rallies like this are retraced, especially if the market has not already made its cyclical low. So, I do not see any reason to rush into AMD here above $132.00, even if the company just reported blowout earnings. Instead, I believe the ideal buy point for the stock is at $100.00 or lower if the stock can re-test or undercut its recent low and its 250-day moving average. In summary, AMD is a great name to put on one's watch-list, but I would not pay up for the stock here.

With the Nasdaq-100 rallying more than 10% from its recent lows and most of the fear from two weeks ago having subsided, I do not believe this is the time to pay up for tech names. Having said that, PYPL has diverged from the group after getting decimated following a brutal Q4 report, and AMD remains a market leader, so any undercuts of its recent support level should provide a buying opportunity. To summarize, while I am not a buyer of PYPL and AMD at current levels (I am long PYPL from $119.50), I would view any pullbacks below $120.00 on PYPL and $100.00 on AMD as buying opportunities.

Disclosure: I am long PYPL

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

PYPL shares were trading at $120.41 per share on Friday morning, up $1.39 (+1.17%). Year-to-date, PYPL has declined -36.15%, versus a -5.22% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor's background, along with links to his most recent articles.

The post 2 Tech Stocks to Buy During the Market Correction appeared first on StockNews.com