Undervalued Spotify Could Be a Bargain as Podcasting Booms InvestorPlace - Stock Market News, Stock Advice & Trading TipsSPOT stock has consistent fundamentals and the podcast business looks promising. However, in a market like this, Spotify might be...

This story originally appeared on InvestorPlace

InvestorPlace - Stock Market News, Stock Advice & Trading Tips

Spotify (NYSE:SPOT) is a growth stock, and unfortunately, growth stocks often bring volatility along with them. Investors need to account for price fluctuations when adding it in their portfolio. Consider that SPOT stock has just an 0.25% total return since its 2018 direct listing on the New York Stock Exchange. But I think it has the potential for significant gains over the next few years.

The no-dividend company currently trades near $147 a share and has a market capitalization of around $28 billion. That is less than half the $69 billion mark of February 2021. Beta is at 1.63, signaling meaningful volatility for SPOT stock investors, as mentioned before. The street anticipates a year-over-year (YoY) sales increase around 20% for this year and 17% for next year.

A SPOT Stock Business Breakdown

The audio streaming giant has built its status through audio distribution, and more specifically, music and podcasts. Spotify has 82 million tracks and 3.6 million podcasts available at the moment. The Joe Rogan Experience podcast addition has been monumental for the podcasting side of the business. SPOT stock had surged by almost $4 billion when Rogan was announced.

Spotify onboards music on its platform and disseminates the audio to its users. The music is sourced from the top music producers, including Sony (NYSE:SONY), Universal and Warner (NASDAQ:WMG). The Stockholm-based company is able to monetize in two major ways: through premium subscription fees and through advertising.

A majority of revenue for SPOT stock comes from premium subscription fees (85%) and the rest comes from advertising-generated revenue (15%). These ratios used to be 90% and 10% in previous quarters. As a rule of thumb, increased streaming time leads to greater engagement and increased engagement leads to greater numbers of premium subscribers and ad revenue. Spotify advertisement revenue comes through audio, video or podcast ads. Audio and podcasting competitors include Apple (NASDAQ:AAPL), Alphabet's (NASDAQ:GOOG, NASDAQ:GOOGL) YouTube and SoundCloud.

In the latest quarter, Spotify increased paid premium subscribers 16% YoY, to 180 million — that's up 8 million from the previous quarter. Monthly active users (MAU) increased by 18% YoY, from 345 million to 406 million users. Average revenue per user (ARPU) has grown at 3% YoY.

Essential Financial Metrics for SPOT stock

Spotify holds a third of the audio streaming market share and is one of the leaders in the growing business of podcasting. Forecasting MAU, growth rate and momentum is a key indicator for future SPOT stock performance.

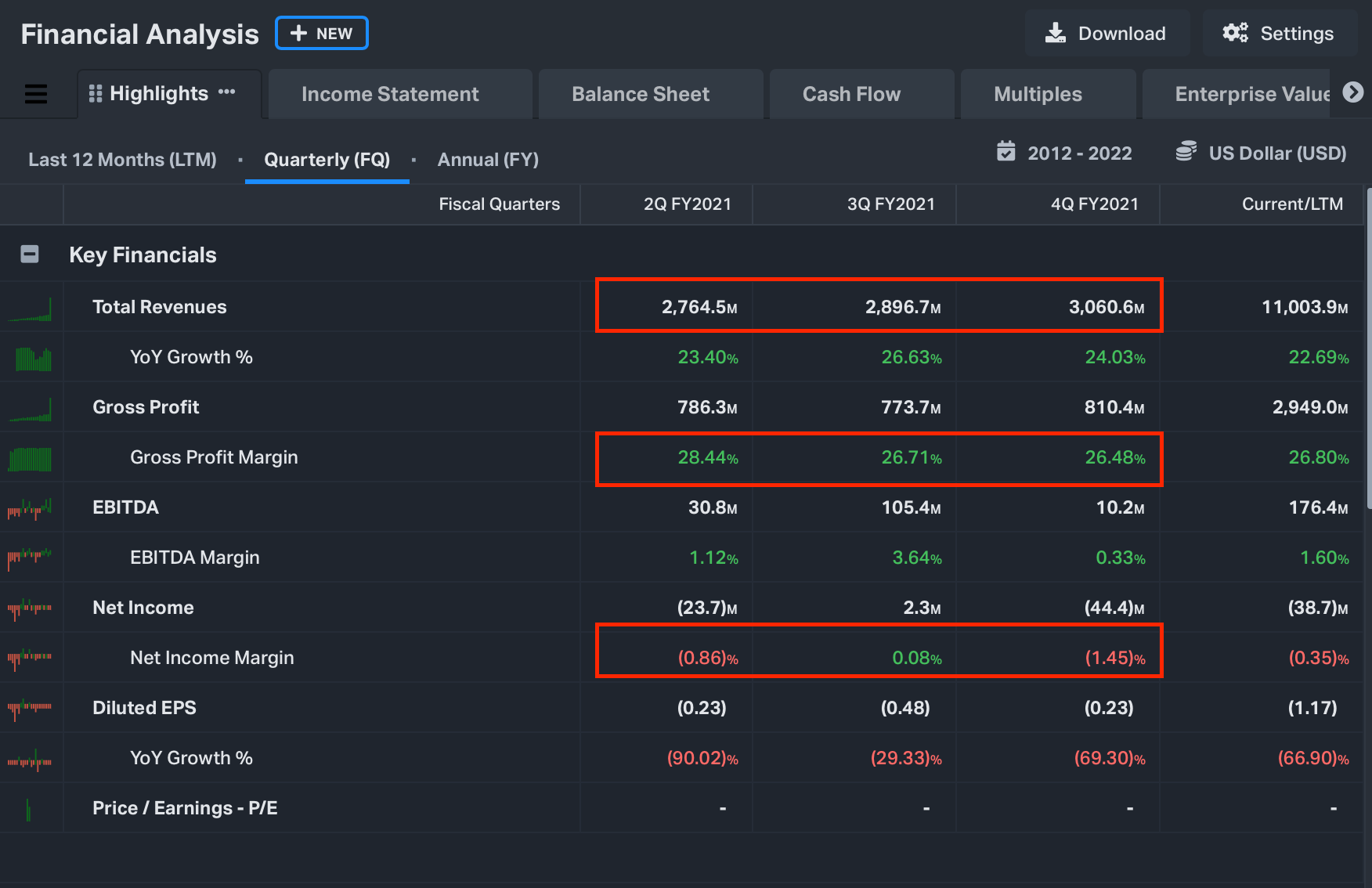

SPOT stock trades around 3x enterprise value/sales, a sensible ratio for a growth stock. Spotify holds $3.1 billion in cash equivalent and $1.3 billion in long term debt. This type of cash balance won't allow the company to compete with gigantic ad competitors and doesn't give room for acquisitions or aggressive expansion. Spotify has a growing free cash flow (FCF) — currently at $117 million and that number has increased every quarter since Q2 2021. And gross margin is over 26%. However the company is struggling with negative net income. Latest earning show -$44.4 million in net income.

The street is now starting to evaluate the changing business model (85%-15% vs 90%-10%) in a different way, as the company is heading into new total addressable markets (TAM).

Needless to say, the audio streaming business has other competitors as well, such as traditional radio. Nevertheless, macro trend indicators reveal that ads spent on radio will decline. The reallocated ad budget will most likely flow into audio streaming, and Spotify is uniquely positioned to capture a good fraction of this budget. In essence, Spotify is competing in a growing landscape.

Spotify Outlook

The present market is volatile and Russia's invasion of Ukraine is further adding to the uncertainty. Investors are cautious in the short term. During troubled or uncertain markets, it is hard for single stocks to outperform the main indices.

On the other hand, the podcast growth trend is optimistic. As long as the podcasting audience keeps growing, and as long as Spotify maintains strong market share and keeps existing margins, then the business should be able to consistently grow. The financials are in fairly good shape and the balance sheet is showing that current assets are in line with payable debts.

One key thing to note is that main revenue comes from North America and Europe, and therefore SPOT stock has to continue growing AMU and ARPU in those regions to remain competitive.

Present valuation is the future cash flows stream, discounted and adjusted. In the case of SPOT stock, I expect future earnings to beat upper-end expectations. The market is in correction territories and it is dragging stocks prices down with it. One challenging aspect is that high growth/high valuation is out of favor at the moment, and that factor could keep the stock down for a while. Despite this, I consider SPOT stock significantly undervalued at the moment, with a relatively strong upside for the next one to three years.

On the date of publication, Jonathan Tang did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Jonathan Tang has gained extensive experience in the financial services industry in London. He has completed valuable projects for companies such as Bloomberg, London Stock Exchange Group and FactSet. He holds a master's degree in Investment & Risk Finance and has completed an MBA course at the London School of Economics. Jonathan has a passion for fintechs that democratize investing, stock market and public equities, ETFs, start-ups and real estate.

More From InvestorPlace

- Stock Prodigy Who Found NIO at $2… Says Buy THIS Now

- Man Who Called Black Monday: "Prepare Now."

- Get in Now on Tiny $3 "Forever Battery' Stock

- Interested in Crypto? Read This First...

The post Undervalued Spotify Could Be a Bargain as Podcasting Booms appeared first on InvestorPlace.