SAP Digital Currency Hub: Transforming Cross-Border Payments Through Digital Currencies Blockchain technology and stablecoins have emerged as powerful solutions to the inefficiencies of traditional payment systems.

Opinions expressed by Entrepreneur contributors are their own.

You're reading Entrepreneur Middle East, an international franchise of Entrepreneur Media.

For decades, the world of cross-border payments has been ripe for disruption. Businesses, particularly small and medium-sized enterprises (SMEs), have long endured high fees, opaque processes, and sluggish transaction times as they navigate international transactions. These inefficiencies have become glaring pain points in today's globalized digital economy, where money needs to move as fast as ideas.

The persistent challenges in cross-border payments

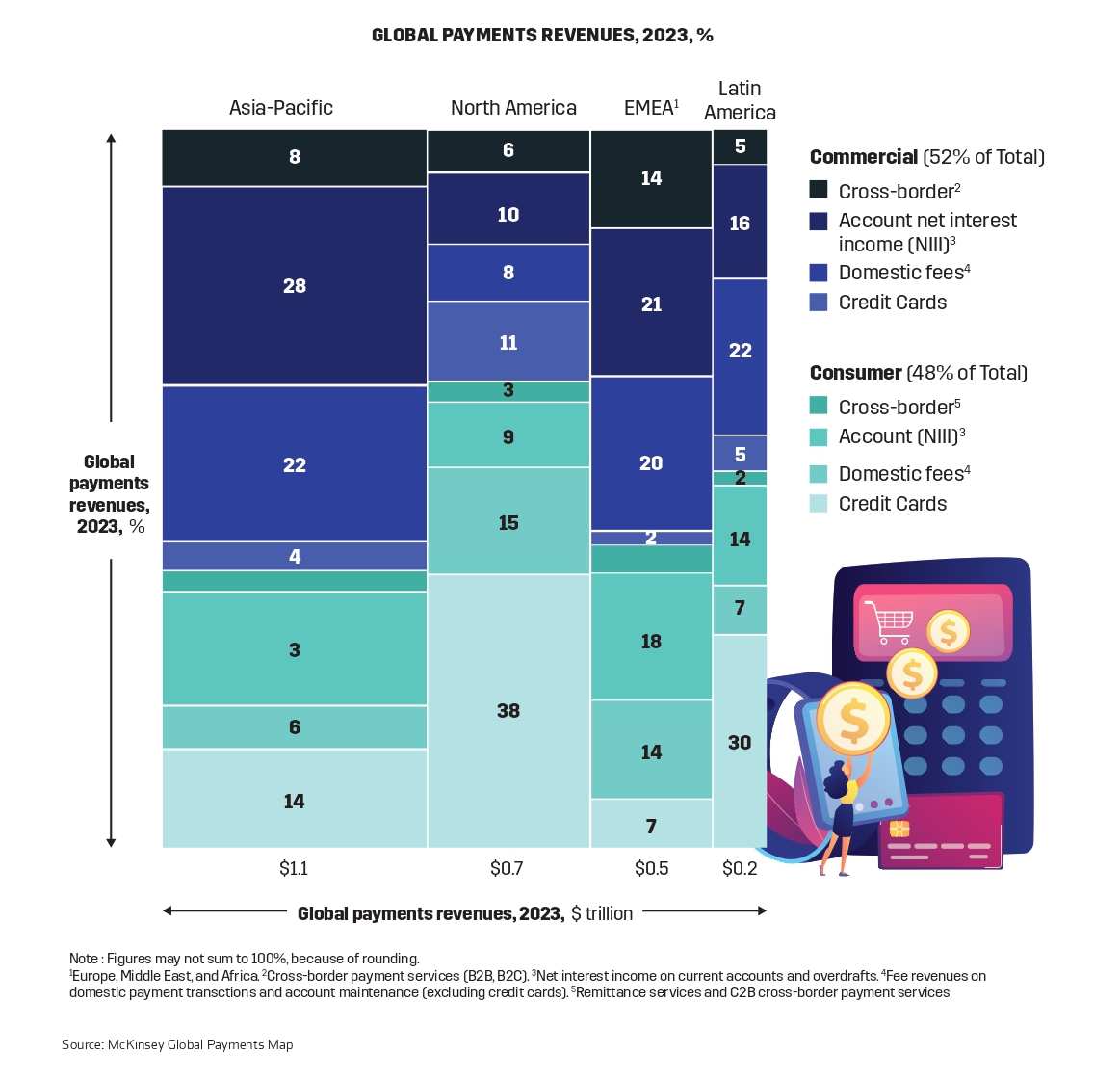

According to McKinsey & Company, the global payments industry processed 3.4 trillion transactions in 2023, representing an astonishing US $1.8 quadrillion in total value.

This activity generated a revenue pool of US $2.4 trillion. Cross-border payments, spanning both consumer and commercial verticals, contributed approximately 12% of these global revenues. Notably, commercial payments dominated this segment, accounting for over 70% of cross-border payment revenues.

The infrastructure supporting crossborder payments was built for a different era and has failed to keep up with the speed, cost-efficiency, and transparency demanded by today's businesses. Companies face five critical challenges that highlight the inefficiencies of traditional systems:

1. High Costs: Sending $100,000 via wire transfer can cost between $150 and $500. Even card-based transactions, like those processed through Visa or Mastercard, typically incur fees of $100 to $300 (based on CryptoCrunchApp). These costs are especially burdensome for SMEs with limited margins.

2. Availability and Delays: Payments often require several days to process, exacerbated by the lack of 24/7 availability. The involvement of multiple banks, currency conversions, and intermediaries further extends processing times. These delays not only disrupt cash flow but also create significant operational challenges for businesses relying on timely transactions.

3. Security Risks: The involvement of multiple intermediaries increases the risk of fraud and cyberattacks. Each additional party in the payment chain represents a potential vulnerability.

4. Liquidity Constraints: Delayed transactions can tie up valuable working capital, leaving businesses unable to reinvest, pay suppliers, or cover day-to-day expenses in a timely manner.

5. Lack of Transparency: The complexity of cross-border payments often leaves businesses uncertain about the status, costs, or timing of transactions. This lack of clarity makes financial planning and reconciliation more difficult.

These challenges disproportionately affect SMEs and startups, especially those operating in emerging markets. In these regions, fragmented regulatory environments and limited banking infrastructure further exacerbate the inefficiencies.

How blockchain and stablecoins are changing the cross-border payment landscape

Blockchain technology and stablecoins have emerged as powerful solutions to the inefficiencies of traditional payment systems. By eliminating intermediaries, blockchain enables near-instant settlement and reduces transaction costs dramatically. Networks like Solana and the Bitcoin Lightning Network exemplify the potential: Solana processes payments for a mere $0.00025 per transaction, while the Bitcoin Lightning Network costs less than $0.01 per transfer.

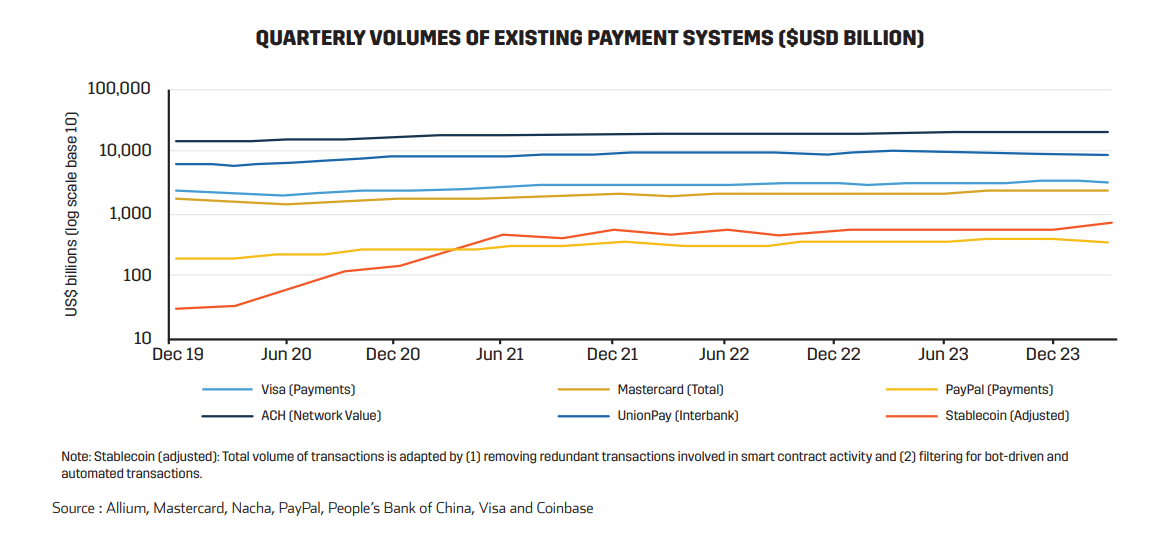

Stablecoins, digital assets pegged to fiat currencies, provide a practical alternative for crossborder transactions by maintaining a stable value. Unlike traditional cryptocurrencies, which are subject to significant price volatility, stablecoins offer predictability, making them particularly useful for payments and remittances. In 2023, stablecoin settlement volumes surpassed US $3.7 trillion globally , reflecting their growing role in the digital economy.

However, when adjusted for "organic" transactions—excluding speculative trading—stablecoins still facilitated over US $2.3 trillion in payments, peer-topeer (P2P) transfers, and remittances. Cross-border business-to-business (B2B) transactions on blockchains accounted for a modest US $843 million within this adjusted total, but this segment is expected to grow significantly, with projections indicating a rise to US $1.2 billion by the end of 2024 (Statista). This growth underscores the increasing adoption of stablecoins as enterprises and individuals seek faster, more cost-effective alternatives to traditional cross-border payment systems. As a result, stablecoin adjusted volume of transactions is rapidly catching up to the likes of Mastercard and Visa global networks.

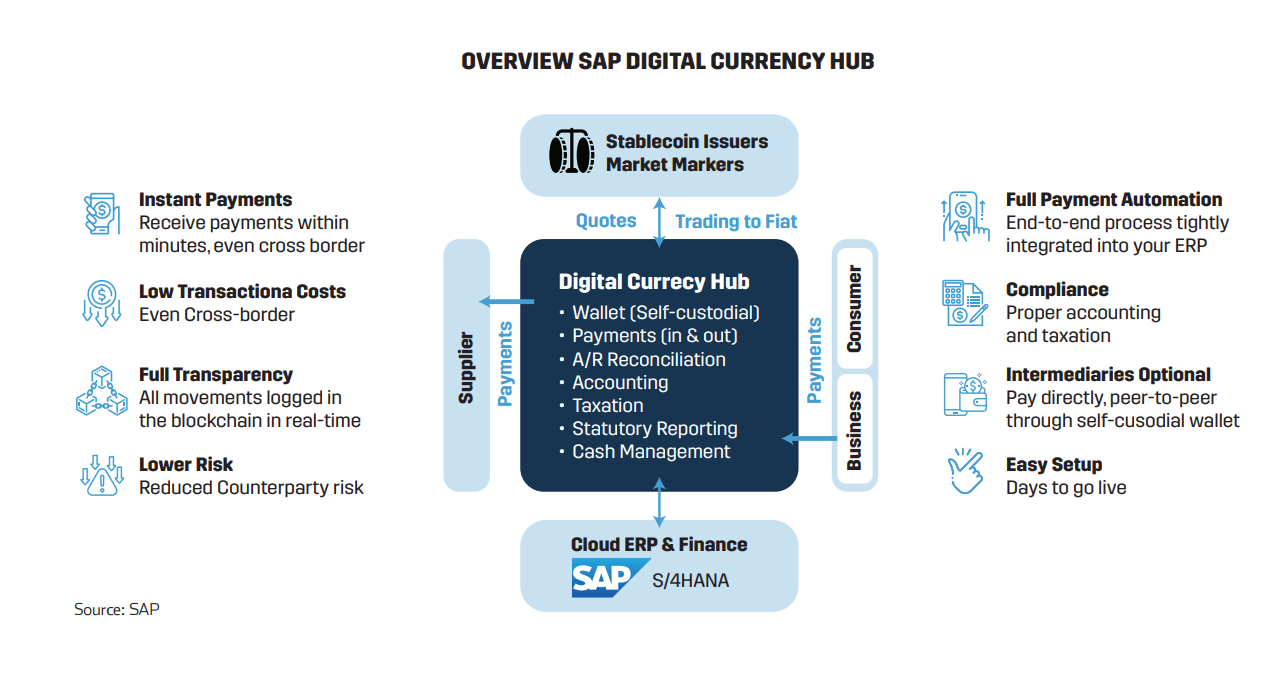

The SAP Digital Currency Hub: Redefining enterprise payments

SAP's Digital Currency Hub is far more than a typical payment platform—it is an enterprise-grade solution designed to seamlessly integrate digital currencies into the financial operations of global businesses. By leveraging stablecoins and blockchain technology, the Hub eliminates inefficiencies in cross-border payments while offering tools tailored to the demands of modern corporations.

Key Capabilities with of SAP Digital Currency Hub

1. 24/7 Instant Payments

The Digital Currency Hub removes the limitations of traditional banking hours, enabling businesses to send and receive payments at any time. This capability ensures smooth operations across time zones, making it particularly valuable for multinational enterprises.

2. Seamless ERP Integration

The platform will directly integrate with SAP S/4HANA Cloud, automating the reconciliation of payments and providing realtime visibility into both fiat and digital currency holdings. This enhanced integration streamlines financial processes, improves cash flow management, and reduces administrative burdens.

3. Multi-Currency and Multi-Network Support

SAP Digital Currency Hub supports leading stablecoins such as USDC and PYUSD, preconfigured for use on blockchain networks like Ethereum and Polygon. Its flexible architecture allows SAPto add additional stablecoins or networks as needed, ensuring adaptability to diverse payment requirements of its customers.

4. Self-Custody Wallets and Fiat Conversion

Businesses can maintain full control of their digital currency holdings through self-custody wallets, eliminating reliance on intermediaries and enhancing security. Alternatively, for organizations that prefer a custody-based model, SAP plans integrations with custody providers to securely store digital assets and manage blockchain transactions through a licensed service provider. The Hub also connects to exchanges for seamless conversions between fiat and digital currencies, simplifying global payment processes.

5. Auditability and Transparency

Blockchain's inherent transparency provides an immutable record of transactions. This capability significantly reduces fraud risks and facilitates compliance with reporting requirements.

A simplified payment process

To utilize SAP's Digital Currency Hub, buyers and suppliers first establish a payment agreement specifying the stablecoin and blockchain network for settlement. For example, current options include PYUSD on Ethereum and USDC on Ethereum or Polygon.

1. Invoice Integration

After the payment run, the ERP sends invoices to the Hub. Rather than routing payment instructions to a traditional bank, the Hub processes them for blockchain settlement.

2. Transaction Execution

• If the enterprise opts for self custody, the Hub generates and signs the blockchain transaction directly, allowing the business to retain full control of its digital assets.

• Alternatively, in a custody-based model, the Hub interfaces with custody providers to execute the transaction on the blockchain.

3. Validation and Reconciliation

Once the blockchain transaction is validated and finalized, the Digital Currency Hub generates an account statement, which is uploaded to the ERP system to reconcile payables and receivables.

This streamlined process ensures that stablecoin payments are as intuitive as traditional bank transfers but offer the added advantages of instant settlement, 24/7 availability, and significantly lower fees.

Real-world proof of concept: PayPal, EY, and SAP Collaboration

SAP Digital Currency Hub was recently showcased in the first real-world transaction involving PayPal and Ernst & Young (EY). In September, PayPal used its PYUSD stablecoin to pay an invoice to EY, leveraging SAP's Digital Currency Hub to facilitate the transaction. The payment, executed on the Ethereum blockchain, was settled instantly and seamlessly integrated into the ERP system for reconciliation.

For PayPal, this transaction highlighted the efficiency and cost-effectiveness of stablecoins in enterprise settings. "The enterprise environment is very well suited for this," said Jose Fernandez da Ponte, PayPal's Senior Vice President of blockchain and digital currency. "It's a very rational conversation to have with the CFO."

The road ahead: bridging innovation and global payment needs

The SAP Digital Currency Hub demonstrates how digital currencies and blockchain technology can reshape cross-border payments, addressing long-standing inefficiencies such as high costs, delays, and lack of transparency. By integrating these technologies into enterprise systems, businesses can achieve faster, more efficient, and more reliable transactions.

The UAE's AED Stablecoin initiative adds another layer of relevance, particularly for SMEs and startups in emerging markets. A regulated, dirham pegged digital currency provides these businesses with a stable, cost-effective tool for international and domestic payments while aligning with local regulatory frameworks. When paired with platforms like SAP Digital Currency Hub, AED Stablecoin and similar initiatives enable enterprises to simplify operations, manage cash flow more effectively, and explore opportunities beyond their home markets.

As digital currencies continue to evolve, the focus shifts from experimentation to adoption. For businesses navigating the complexities of globalization, tools that integrate digital currencies into everyday financial processes will become critical. Initiatives like AED Stablecoin—and platforms capable of leveraging them—signal the direction of travel for the future of global payments.

Explore the transformative trends shaping the Middle East's Fintech sector. Read or download your copy of "The State of Fintech in the Middle East" now.

This article was originally published on Lucidity Insights, a partner of Entrepreneur Middle East in developing special reports on the Middle East and Africa's tech and entrepreneurial ecosystems.