Retirement Does Not Exempt You From Taxes: How to Prepare for It Retirement is a significant milestone for workers, especially those who are happy to reach their golden years. Upon receiving your last salary, you can start sleeping soundly. You don't have...

This story originally appeared on Due

Retirement is a significant milestone for workers, especially those who are happy to reach their golden years. Upon receiving your last salary, you can start sleeping soundly. You don't have to bother setting the alarm for your nine-to-five job. You will no longer have to go through the hassle of commuting and getting stuck in traffic. Even if it's a remote job, you will no longer have to drag yourself out of bed and face your laptop. At least, this is the dream of those of us dreaming of this great day.

Legally You Can Retire at 66 — But There is Not a Minimum Age

Indeed, retirement is sweet, as you can finally enjoy your free time. You can travel whenever and wherever. You can go to the salon and mall to relieve your stress. You can stay up late at night to watch your favorite Netflix series.

Most of all, you can catch up with your loved ones after all the deadlines you had to prioritize. The thing is, retirement does not have a minimum age, although legally, it's 66. It's up to you to retire even in your twenties and start your dream business.

Income Taxes Do Not End With Payslips

But hold your horses. Retirement may be tempting and promising, but income taxes do not end with payslips, meaning you will still be considered a taxpayer even when you're no longer working. Retirement tax rates can reduce the amount in an individual retirement account. To that end, you must have careful retirement planning before filling out your SSA-1 form.

Thankfully, there are many clever ways to prepare your finances before retiring. You can ease the tax burden on tax-deferred investments, retirement savings, and pensions. Even better, you can increase your sources of income to enjoy worry-free retirement years. This article will provide some tax strategies to get the retirement income you want.

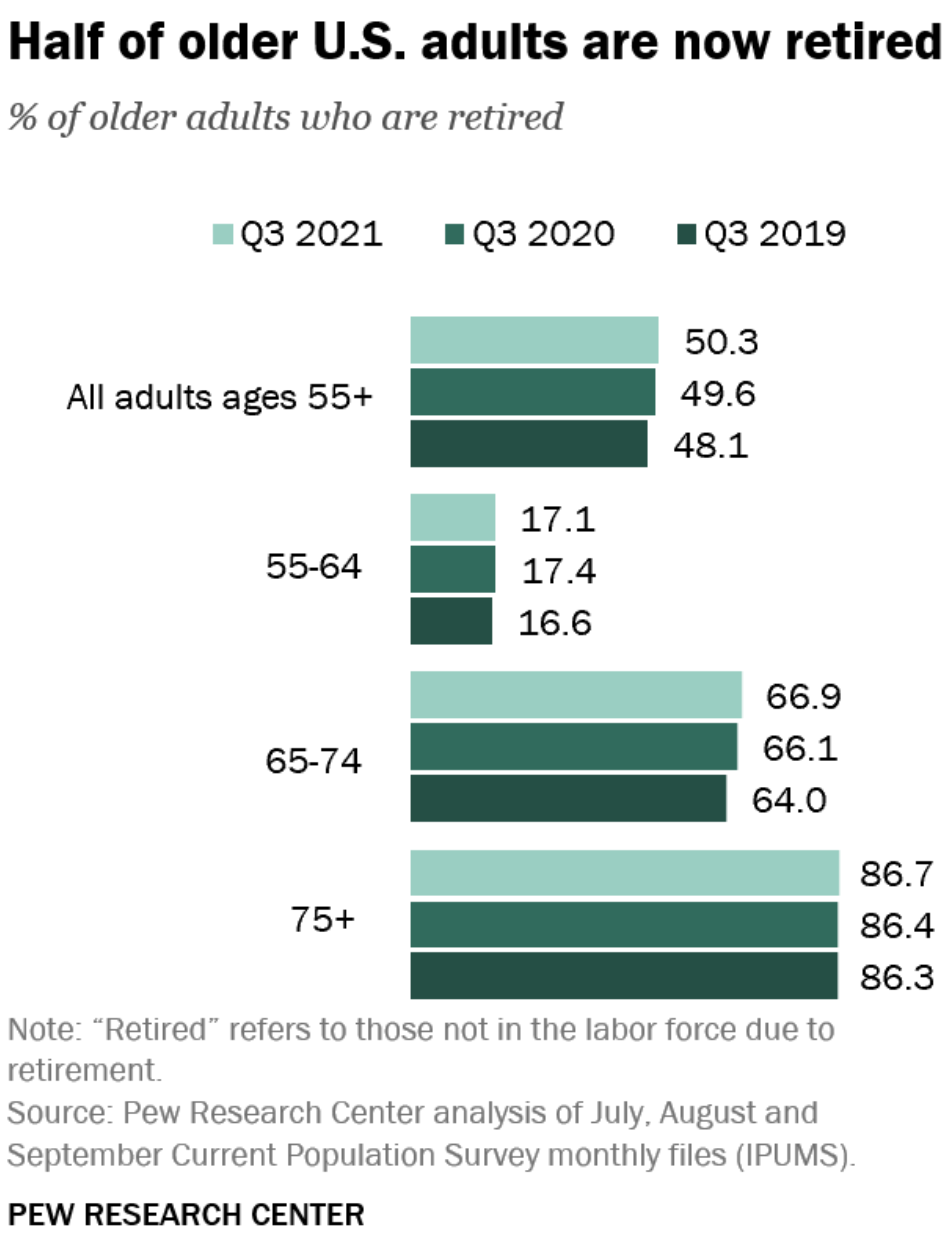

The State of Retirement in the US

Nothing in the retirement rule book says you should work until you turn 66 or 67. In fact, about half of workers in their mid-50s have retired in the last three years. Others aim to retire as early as 40 years old. Despite this, the Great Recession's scar has remained visible over the years. Sadly, many would-be retirees had to tap into their savings accounts to meet daily expenses. Meanwhile, many seniors and retirees have depleted their savings and lived in debt. So if there's one great lesson we got from the crisis, it's to prepare for retirement.

Take Advantage of Financial Planning

In 2021, financial planning was already at the forefront of literacy and resilience among Americans. Although there was an inequality in retirement account ownership, it was still a massive improvement from the past decade. Unsurprisingly, many younger workers became more cautious of market volatility.

Shocks were more evident in low-income households, leading us to look for more income streams. Businesses and policymakers have already learned the hard way as well. That might be why we quickly regained footing after the pandemic recession.

But not a year later, the picture now seems bland. Although the labor market conditions are still a far cry from the Great Recession, older adults don't want to take chances. They no longer mind working longer to put more taxable income into their retirement savings account.

Recent data show that more than one-third of private sector employees expected retirement delays. Indeed, inflation has already stretched beyond expectation. Even if it is starting to relax at 6.5%, it is still far higher than pre-pandemic rates. As such, 66% of employees cited inflation as the primary hindrance to their retirement. It is a substantial increase from 51% in 2021.

Shifts in Retirement Plans Can Lead to Indirect Costs — Watch These!

Moreover, this sudden shift in retirement plans has led to more indirect costs. For instance, 22% of employers saw the negative impact of retirement delays on the physical health of employees. Nearly 30% saw its effect on their mental health, resulting in lower workforce productivity. In addition, 34% said it also delayed the promotion of younger workers.

Despite all these, 24% of would-be retirees said retiring soon could be a disaster. The skyrocketing cost of goods and interest rates might push them to bankruptcy. This response proves that the actual value is still meager despite the increased retirement account ownership. The only consolation is that they have a few thousand dollars to use before touching their savings.

How Retirement Income Is Taxed

As a retiree, taxes can take away a considerable portion of your income, leaving you with less to spend and save. So, you must remember that taxes can still haunt you even if you retire. Nevertheless, you can do something as early as now to lessen your Internal Revenue Service (IRS) notices later.

Tax Rules Remain Difficult to Understand

Tax rules can be complex, so you must familiarize yourself with them while still working. Doing so can help you cut or reduce tax bills in your retirement years. This part will discuss the primary sources of retirement and how they are taxed.

The first thing to consider is your retirement tax bracket. It is basically the same as determining tax brackets in your working years. Your tax return filing status and adjusted gross income point you to the appropriate bracket. You can find tax tables with corresponding federal income tax rates online.

But before proceeding, know that income tax rates are variable since the IRS adjusts them to inflation. Tax reform legislation can also increase or decrease them. With that, retirement income taxes can be tough to predict. Still, you can get a rough idea of your tax bracket upon estimating your retirement income.

Traditional IRA and 401 (k) Withdrawals

Traditional Individual Retirement Account (IRA) and 401 (k) withdrawals are taxed just like ordinary income. You may face a tax penalty if you do not get the required minimum distributions (RMDs). It is equivalent to 50% of the unwithdrawn amount. So take your required minimum distribution to keep the tax penalty away from your retirement income.

Certain circumstances may allow you to withhold taxes on your IRA and 401 (k) distributions. Some 401 (k) plans use this tax mechanism as their default. So they become tax-deferred accounts. If you do not pay taxes on your withdrawals, the IRS may require you to pay estimated quarterly taxes. The agency will ensure you regularly pay the owed amount.

Social Security Benefits

Federal income taxes may apply to your social security benefits. It happens when your provisional income is higher than the respective threshold per filing status. Provisional income is 50% of all taxable income, certain non-taxable income like municipal bond interest and social security benefits. Based on the table below, you can see how taxes apply to social security benefits with respect to your provisional income.

| Percentage of Benefits Subject to Taxes | Marriage Joint Filers | Other Filing Status |

| 0% | $0-31,999 | $0-$24,999 |

| Maximum of 50% | $32,000-44,000 | $25,000-34,000 |

| Maximum of 80% | $44,001 and above | $34,001 and above |

Moreover, you can request the Social Security Administration to withhold your taxes from your check like employers do. That way, you will not end up paying overwhelming taxes to the IRS upon filing. Otherwise, you may have to file quarterly estimated returns throughout the tax year.

Investment Income

Even if you file your retirement, you may still have other sources of income. Investments are a typical option, but they may be part of taxable accounts. Since investment securities have different natures, different rules may also apply. Here are the common sources of investment income.

Interest Income

Interest income often comes from debt securities, such as corporate, treasury, and municipal bonds. Mortgage-backed securities, certificates of deposits (CDs), and interest on checking or savings accounts also yield interest. Ordinary tax rates apply to them.

Dividend Income

Dividend income is often subject to preferential rates for taxation. It must meet the minimum criteria. First, dividends must come from your shares or holdings in the US and qualified publicly-traded or private companies. Second, you must be holding your dividend-paying stock for a certain minimum period.

Note that the management may distribute dividends every quarter or half-year. But payouts are more consistent in private companies. So if the company does not distribute dividends, no taxes will apply. Meanwhile, your ordinary income tax rate will apply if dividends are unqualified.

Income from Gains on an Investment Sale

You receive investment sale gains when the fair value upon selling it exceeds the fair value when you buy it. It covers all forms of investments, such as stocks, bonds, and fixed assets. If you sell them a year and a day after the acquisition, the long-term capital gains tax rate will apply. If the sale happens in the same year, the short-term capital gains tax rate will apply. It is the same as your ordinary income tax rate.

On the other hand, if you incur capital losses, you will not have to think about taxes. Also, the IRS allows individuals to offset ordinary income by up to $3,000 per year. And any additional capital losses can be carried forward.

Tax Strategies for Your Retirement Income

I bet you're not keen about forking any part of your income to Uncle Sam. Your hesitation and defiance may intensify once you retire because you may not have enough income streams. Also, your avoidance tendencies in your golden years are logical. Imagine yourself regularly paying or receiving letters from the IRS. These taxes will be taken away from your retirement income or savings- a portion you set aside for your golden years. Remember all the cravings you had to repress and all your travel plans to postpone to maintain your savings.

Don't worry. I am not telling you to commit tax evasion or avoidance. We don't want to incur a tax penalty that may divide your retirement income into two. On a lighter note, there are some strategies you can apply to eliminate or at least lower your tax bill. Even tax professionals know these and can guarantee the legality of these steps. Of course, the success of our plans requires some effort in advance.

1. Move to a more tax-friendly state

It may sound desperate, but this decision is optimal and tax-efficient. Often, states with higher taxes have a more active business sector. In turn, the standard of living also tends to be higher.

Suppose you are living in Hawaii. It may be expensive for you, given the average income tax rate of 11% and the cost of living index of 189.9. Indeed, the enchanting scenery comes at a high price. It may be difficult for retirees to cover exorbitant living expenses and taxes.

Know that your job can no longer limit your geographic location after retirement. It pays to be wiser and braver. Starting anew in a place where you won't have to worry about skyrocketing costs may also keep you away from stress and improve your mental health.

2. Go for tax-exempt or tax-friendly investments

It is not uncommon to see retirees moving a portion of their investments to bonds. Doing so helps them maintain their risk tolerance as they age. It is more crucial today as macroeconomic volatility persists. Historically, retirees have been vulnerable to massive economic crises. It forced them to deplete their savings or live for another twenty years stuck in personal and mortgage loans.

Debt securities like bonds are still subject to tax since they yield interest. But some types offer a more favorable tax rule. For example, treasury bonds are often exempt from state and local taxes.

Meanwhile, municipal bonds are not subject to federal taxes. States, counties, and cities issue these bonds to finance projects. They are different from corporate bonds, which companies issue. But they work the same since they all act as financial leverage for the issuer.

Overall, bonds issued by public institutions have very low tax rates or even nil. The story is different if you buy municipal bonds in another state. In that case, you will pay their state income taxes.

Dividend stocks can also be optimal if you wish to generate higher yields with manageable risk levels. You will not have to bother checking the stock price every minute to buy and sell stocks. All you need to do is find a stock with consistent dividend payouts at a reasonable price.

You can use the dividend yield by dividing the annualized value of dividends by the stock price. It is easier in publicly-traded companies since you can find all the information on the internet.

Check Out Several Choices Before the Final Decision

I suggest OneMain Financial Holdings, Inc. (OMF), with a dividend yield of 8.12%. For more choices, check the rare list of Dividend Champions. These stocks have been distributing dividends for at least 25 consecutive years. You can also consider the Dividend Contenders and Challengers.

They are relatively newer, but they have the potential to get on the Dividend Champion list. Even better, you opt to buy foreign dividend-paying stocks. Both of these stocks have more enticing tax rates, which can only be 20%, 15%, or even 0%.

Of course, it depends on your taxable income. If you want an investment with more balanced risks and yields, mutual funds can be an excellent choice. Mutual funds can derive solid returns like stocks, but they are safer.

3. Choose Roth Accounts

Roth IRA and Roth 401 (k) offer tax-free distributions upon retirement. You can get as much money out of Roth accounts without paying taxes if you follow the IRS withdrawal rules. As such, you can use them as your primary or secondary retirement account to avoid or reduce tax bills.

Moreover, Roth does not give an up-front tax break in the same year you pay contributions. As such, you can choose Roths if your expected retirement tax bracket is higher than in your working years.

You can convert traditional IRA or 401 (k) accounts but beware of tax consequences. Also, a five-year rule might limit the accessibility of your tax-free funds. So, you must roll over your account five years before retirement.

4. Make and adhere to your withdrawal strategies

When you turn 73, you must start taking RMDs from your traditional IRA and 401 (k) accounts. The amount depends on your age and account balance. But there's more than meets the eye because you can have your withdrawal strategy. For instance, you can take larger taxable distributions when you expect your income to decrease. That way, the equivalent tax rate on your distributions will also be lower.

It may be better to delay your RMDs, so you won't have to pay taxes. But note that there's a $100,000 limit every year. You must ask your IRA custodian to transfer the funds directly to one of the IRS-approved charities. Also, you must receive an acknowledgment from the charity.

5. Choose between insurance and annuities

While it's pleasing to see your hard-earned money in your retirement savings account, it's better to have an extra layer of security. That's where insurance and annuities enter the scene. Your retirement income can cover all your living expenses every month. But it can't always be sufficient for emergencies like accidents and hospitalizations. It can't also perpetually guarantee assisted living costs. Even medicare may not be enough to pay all your hospital bills.

Check Your Coverage

Many research shows that individuals aged 65 and above may have a weaker immune system. They cover the vast majority of those getting hospitalized. With that, you must have the means to protect your income and savings. Also, climate change intensifies, which may lead to property destruction. We have already seen the damages brought upon by Hurricane Ida and Ian. Today, insurance and annuities are at the forefront of financial literacy and resilience.

Insurance and annuities are similar in that policyholders must pay premiums regularly. Many reliable financial advisors are affiliated with insurance companies. So you can ask for all the information you must understand before buying a policy. Their difference is that life insurance pays policyholders after their death. Meanwhile, annuities pay policyholders as long as they live. But if your sole purpose is to cover hospitalizations, health insurance may be a great fit for you.

Learn More About Retirement Taxes

A consistent income stream has become more crucial than ever before for retirees. Historically, economic crises have depleted wealth in the wink of an eye. And since we're facing macroeconomic volatility, we must protect our finances by all means. More importantly, we must prepare for retirement taxes to preserve the value of our money. Annuities, investments, and insurance can help in more ways than we think.

Tax retirement preparation can be tedious and tricky. Yet, you can achieve your goals with adequate and proper knowledge and strategies.

The post Retirement Does Not Exempt You From Taxes: How to Prepare for It appeared first on Due.